Strengthening Protection for Platform Workers: CPF and Insurance

CPF Contributions - Improving housing and retirement adequacy

The Ministry of Manpower announced that from the second half of 2024, platform workers under the age of 30 are required to contribute to their Ordinary Account (OA) and Special Account (SA). Those who are 30 and above have the option to contribute to their CPF if they wish. Platform workers who earn $500 or less in a month do not need to make CPF contributions.

At least 73,000 platform workers are expected to benefit from this policy. The CPF contribution rates will be gradually phased in over five years, reaching the same level as the contribution rates for traditional employees in 2028.

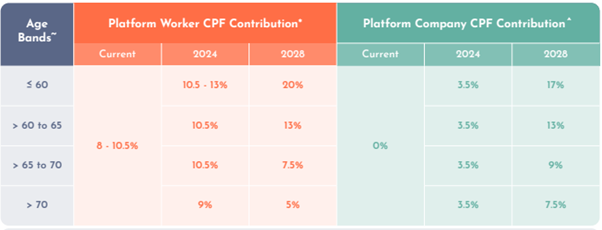

All platform workers currently contribute between 8% and 10.5% of their income into their Medisave account only.

When the policy kicks in later this year, platform workers will start contributing an additional 2.5% of their income. The additional contribution will go into their Ordinary and Special Accounts. This will bring their total CPF contributions to between 10.5% and 13%.

The CPF contribution rate will increase by about 2.5% each year, until it reaches the same rate as traditional full-time employees for their age group. For example, platform workers aged 60 or younger will eventually contribute 20% of their income into their CPF accounts in 2028.

At the same time, platform companies will also make contributions to their workers CPF. The rate will start off with a 3.5% contribution in 2024, increasing about 3.5% a year until 2028. Using the same example, for a platform worker aged 60 or younger, the platform company will make a 17% contribution to the worker’s CPF in 2028.

Reference: Table extracted from Ministry of Manpower. URL: https://www.mom.gov.sg/-/media/mom/documents/budget2023/infographic-on-platform-workers.pdf , retrieved on 19 April 2024.